1. Introduction

SBA is a new capital allowance for construction costs incurred on or after 29 October 2018, at an annual rate of 2 percent (flat rate) on a straight-line basis off their profits before they pay tax. Effectively written down over 50 years.

Rate changed from 2 percent per annum to 3 percent per annum from 1 April 2020 (corporation tax) and 6th April 2020 (Income Tax). As a result, the period over which expenditure may be relieved is reduced from 50 years to 33 and one third years. (see point 3 for example)

2. Leases

Expenditure on constructing a building may be incurred at different times or by different people. We need to apply SBA to each part of expenditure separately.

See an example on HMRC website – CA90350

2.1 Landlord Expenditure

In hospitality trade usually restaurants operate from leasehold premises. Landlord may have spent lot of money in construction or acquisition of the building and lessee maybe interested in knowing whether they can claim any SBA on this expenditure.

Short answer is no. Lessee cannot claim SBA on landlord’s expenditure; we will see the reasons for it below:

Right to claim SBA does not pass to lessee unless both of the following conditions are met:

- the lease term granted is for 35 years or more

- the market value of the lessor’s retained interest in the property is less than one third of the capital sum paid for the grant of the lease – see example (CA90600)

2.2 Leaseholder expenditure

Where leaseholder incurs expenditure usually in fit out of the restaurant, they are eligible to claim SBA on it.

2.3 What happens if lease is terminated?

We currently being in COVID crises will see lot of leases being terminated due to non-payment of rent. Can Landlord’s claim SBA on expenditure incurred by lessee ?

Answer – No (see CA90800)

2.4 What happens if restaurant is sold?

Purchase will step in Seller’s shoe and continue claiming SBA (see CA91010 and CA91400)

Purchase must collect SBA Allowance Statement from Seller.

3. Claiming SBA

Step 1: Identify qualifying expenditure? (see CA93110 and CA93400 and CA94000)

We also need to retain evidence of construction expenditure, such as invoices. Plus retain relevant documents to support the date of earliest construction contract.

Step 2: Prepare Allowance Statement (see CA94610)

This a MUST before SBA is claimed. Where there is no allowance statement, the qualifying expenditure is nil.

Where the current owner incurred the qualifying expenditure in relation to the building, the current owner creates the allowance statement.

Where the current owner acquired the relevant interest in the building from another person, they must obtain the allowance statement from a previous owner.

Evidence requirement: HMRC example of Allowance Statement (CA94560)

| Information to identify the building to which it relates | Unit X |

| Date of first construction contract | 1st January 2020 |

| Total amount of qualifying expenditure | £700,000 |

| Date the building came into use (date from which we start claiming SBA) | 1st March 2020 |

There is no requirement to record the amount of SBA claimed. Any unclaimed SBA cannot be carried forward and is lost, so it is assumed the full amount of SBA available in any period has been claimed.

The amount of the allowance is reduced if the building was brought into qualifying use part way through a year (CA91400).

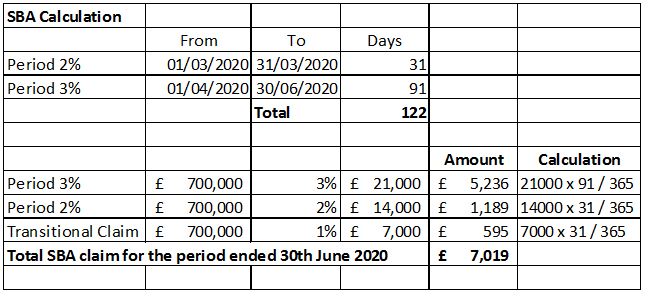

Step 3: Quantify SBA (CA91400)

Suppose it’s a Ltd company which did the expenditure in Step 2 and wishes to claim SBA. It closes its books on 30th June 2020. We calculate the SBA below:

Claim Period: 1st March 2020 to 30th June 2020.

4. Details of Transitional Provisions:

Adjustment for pre-April 2020 allowance: (section 270GD of CAA2001)

read subsection 2 and 3

Source:

HMRC Manual