Leases attract Stamp Duty Land Tax (SDLT).

Sometimes a new lease is signed for the same property before the old lease expires, example when a lease is extended.

In such cases a relief called Overlap relief is available to avoid double taxation. A better back ground to overlap relief is given in SDLTM16010.

Given below is an example of calculation of this overlap relief with an spreadsheet attached which may help tax practitioners.

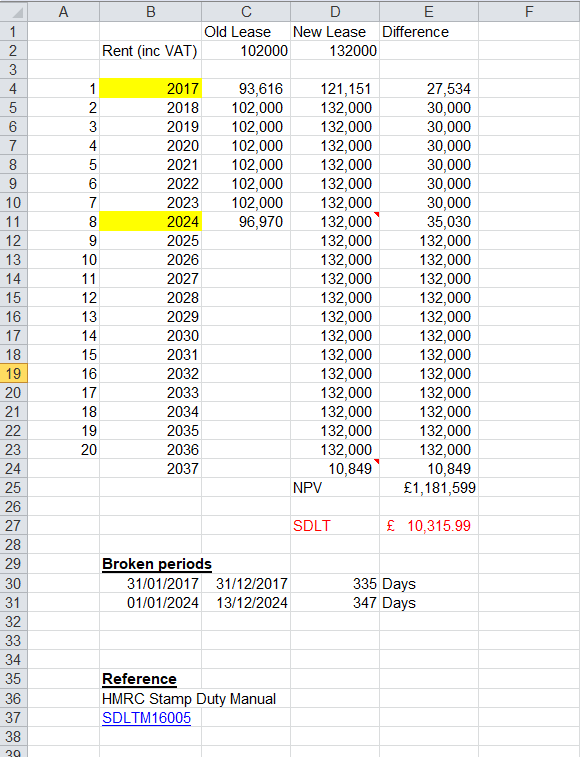

Current lease details:

Start date 14th Dec 2009

Lease term 15 years

End date 13th Dec 2024

Rent £85k + VAT = £102k

New Lease details:

Start date 31st Jan 2017

Lease term 20 years

End date 30th Jan 2037

Rent £110k + VAT = £132k

Below is the screen shot calculation of the SDLT payable.

To download the excel file click here – SDLT Overlap relief calculation